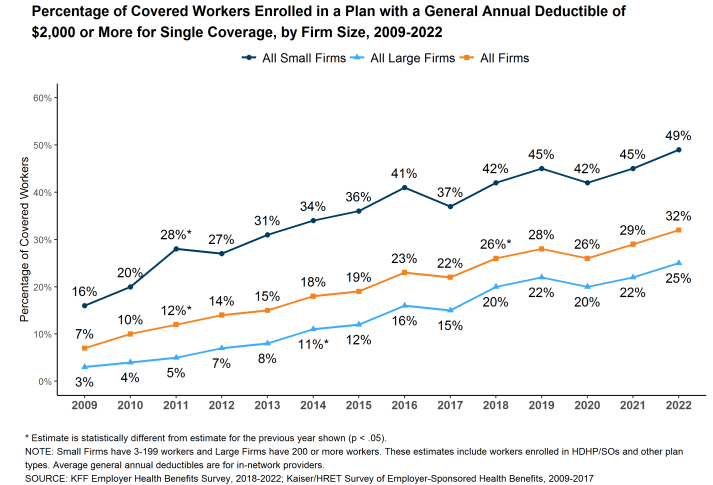

Copay playing cards are considerably controversial. These playing cards or coupons are used to assist sufferers afford copayments and deductible funds sufferers owe when utilizing prescription drugs. On the one hand, these applications are extremely useful for sufferers. Affected person out-of-pocket prices have risen dramatically in recent times, even among the many insured. As an example, whereas solely 7% of employees had a deductible of $2000 or extra in 2009, now 32% have such a excessive deductible. Furthermore, practically half of employees in small companies have a deductible of $2000 or extra. Alternatively, payers declare that copayment playing cards improve well being care prices by growing use of prescription drugs resulting from ethical hazard.

To deal with the problem, payers have began to implement copay adjustment program (CAP), similar to

copay accumulators and copay maximizers.

In accumulator applications, the funds made with copay playing cards don’t rely in opposition to the sufferers’ deductibles or the OOP [out-of-pocket] value maximums. Subsequently, these applications might improve the sufferers’ whole cost-sharing burden and probably result in surprising, substantial midyear bills.

In maximizer applications, the whole annual profit is allowed to extend as much as the utmost quantity {that a} producer is prepared to reimburse sufferers for his or her copay expense. This quantity is distributed throughout a affected person’s profit yr to equalize the usage of these out there funds. These maximizer applications nonetheless don’t rely towards a affected person’s deductible or OOP value most inside a given yr and might delay a affected person’s capability to succeed in this profit threshold, leaving the affected person uncovered to additional prices associated to different drugs or sicknesses.

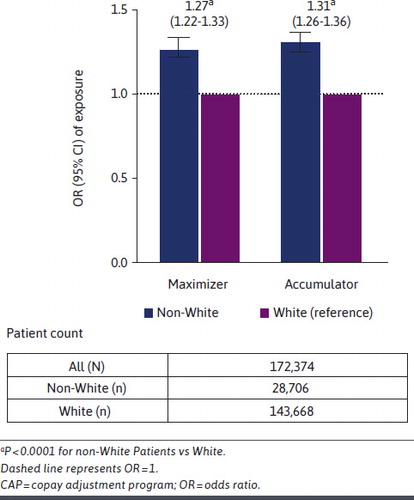

One essential query is whether or not (i) copayment card use varies by racial and ethnic group and (ii) whether or not CAP applications range by racial and ethnic group. That is precisely the analysis query Ingham et al. (2023) intention to reply. The authors use 2019-2021 information from the IQVIA Longitudinal Entry and Adjudication Knowledge (LAAD) 1:1 matched to Experian Advertising Options, LLC shopper information. The previous is a claims information supply, the latter is shopper information supply. Utilizing these information information, the authors discover that:

…there have been no vital variations in copay card utilization between non-White sufferers and White sufferers (odds ratio [OR] = 0.995, 95% CI = 0.99-1.00; P = 0.0964). Nevertheless, amongst copay card customers, non-White sufferers have been considerably extra more likely to be uncovered to CAPs, as both maximizers (OR = 1.27, 95% CI = 1.22-1.33; P < 0.0001) or accumulators (OR = 1.31, 95% CI = 1.26-1.36; P < 0.0001), in contrast with White sufferers.

In different phrases, non-White sufferers are about 30% extra more likely to be uncovered to a CAP program than Whites. The total article is on the market right here.

{kind=link}